Charles Hugh Smith – YOLO spending–grabbing what you can right now because You Only Live Once–is now embedded in the zeitgeist. The original narrative–that the pandemic shutdown awakened a broad cultural awareness of the fragility of life and security, and so it’s wiser to buy experiences now rather than later–may be expanding into the complex realm of inflation and inflation expectations.

Charles Hugh Smith – YOLO spending–grabbing what you can right now because You Only Live Once–is now embedded in the zeitgeist. The original narrative–that the pandemic shutdown awakened a broad cultural awareness of the fragility of life and security, and so it’s wiser to buy experiences now rather than later–may be expanding into the complex realm of inflation and inflation expectations.

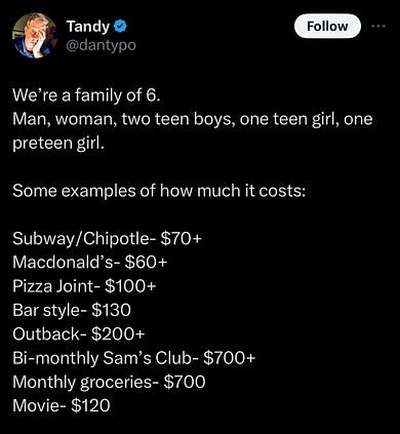

Covid changed how we spend: More YOLO splurging but less saving

The possibility that the human herd senses trend changes before statistics and the economic punditry comes under the capacious category of the wisdom of crowds: in this line of thinking, YOLO spending may be a reflection not just of a pandemic-instigated change of priorities, but of a growing sense that inflation is now embedded, and so it’s better to spend earnings now before they lose value.

This is the core behavioral response to embedded inflation: borrow and spend now, as savings will only lose purchasing power as time goes on. In hyper-inflationary economies, this leads to wage earners finding something to buy the day they’re paid, as their wages will lose value literally overnight.

Put another way, embedded inflation is systemic financial insecurity: the future value of labor and savings is unknown and unknowable, and could be much lower than we expect. To trust that labor and “money” will retain their current purchasing power is a fool’s game, as the crowd intuitively grasps the runaway-feedback nature of inflation: once it gets going, every increase in inflation fuels further increases.

Once this feedback is embedded in our expectations, it becomes extremely difficult to rebuild trust in future valuations of labor and “money.” In other words, there is a psychological element in inflation that is completely real and completely outside actual material causes of inflation such as scarcity and the relentless expansion of the money supply / credit.

Once expectations of inflation become embedded, enterprises raise prices and workers demand higher wages regardless of actual inflationary pressures. The gaslighting manipulation of inflation statistics pours gasoline on the fire of the expectations of inflation, as being told costs only rose 2% when we know they rose 20% destroys confidence in official assurances that “inflation is falling.”

The human herd also intuits that prices never fall back to pre-inflationary-spiral levels. If inflation moderates after a 20% spike, costs across the entire spectrum don’t drop 20%; they simply rise at a slower pace.

Unlike a direct tax, inflation’s indirect tax is difficult to calculate. Income and sales taxes are visible and can be estimated / calculated. The indirect tax of inflation is inherently difficult to estimate, as costs rise at different rates across goods and services, some are stickier than others, etc.

The ravages wrought by future inflation are known unknowns: we know inflation is built into our debt-based economy, but we have no way of knowing its future impact.

The safest approach is to spend cash now before it loses more value. This insecurity feeds back into our confidence in the entire economic status quo: our confidence in our future earnings and job security also decays, strengthening the impetus to spend now because we understand we might not be able to afford the travel, experiences, etc. in the future.

To the authorities and pundits tasked with gaslighting inflation to limit inflationary expectations, the wisdom of crowds looks like the madness of crowds: with trust and confidence in the future value of labor and “money” both declining, the sense of insecurity increases, generating demands for higher wages and prices now rather than later. This feedback loop generates its own inflationary pressure, which then feeds back into itself as everyone grasps the potential for an inflationary spiral that gets out of control.

To the authorities and pundits tasked with reassuring us that inflation is receding, this mob-generated expansion of inflationary feedback is madness. If only everyone believed us that inflation was near-zero, inflation would be near-zero. This is the end result of the idea that if we control expectations, beliefs and perceptions, we can control the real-world economy.

The problem with this idea is all the efforts to control the narrative generate their own feedback: a loss of trust and confidence in the system and its statistics. The harder the authorities and pundits push the “inflation is under control” narrative, the faster they erode public trust and confidence in the future value of labor and “money,” because claiming inflation is 3% and heading down after inflation has burned off 20% of our purchasing power in three years is, well, not credible.

Are we witnessing the wisdom of crowds or the madness of crowds? The old saying money talks, bull-dung walks comes to mind. When our earnings and savings start buying more of everything rather than less, we’ll recalibrate our expectations. Until then, it’s looking like the wisdom of crowds is manifesting.

SF Source Of Two Minds Apr 2024

The thing that shocks me about all of these discussions is the lack of the word “Cumulative”. When we are told inflation is 2% when we feel it is 20% is natural because inflation is cumulative. The rate compounds like interest in a savings account but in the opposite direction. Why is this not discussed?

The experts love showing that chart of inflation starting at under 2% in 2020, peaking in 2022 at over 9%, and now back to about 3%. They say things are much better without saying the net affect is closer to 19%. So, it not takes $5 to buy $4 of 2020 goods. That is not going away….ever! Inflation is only countered by deflation and the experts hate deflation. They tell us a little inflation is great because it means we have a stable economy. So, inflation is designed into our system…and it is cumulative. Why not say it?

Government is the problem. More correctly, bad government is at fault. We cannot print money faster than our productivity offsets the spending. The Democrat party fails to believe this as well as the RINOs. That is why we are suffering today in my opinion.

“Government is the problem.” That pretty much sums it up. That’s why this upcoming US election is so very important – not just for America but for the entire world. -g